Muhammad Sanusi II, emir of Kano and former governor of the Central Bank of Nigeria (CBN), has recommended steps President Muhammadu Buhari must take to revive the Nigerian economy.

In a document acquired by TheCable, as presented at the meetings of the Joint Planning Board (JPB) and National Council on Development Planning (NCDP), Sanusi highlighted the problems with economy, proffering solutions for the Buhari-led admin.

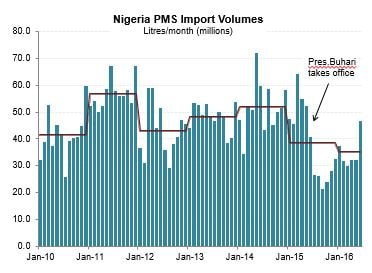

ELIMINATE WASTEFUL AND ABUSE-PRONE SUBSIDIES

Sanusi highlighted the abuse of subsidies in Nigeria and the need to totally put an end to subsidy regimes. He applauded Buhari for the steps taken so far on subsidy, which has become visible in Nigeria’s consumption pattern.

“The Buhari administration has already made great progress in stopping the fraud associated with the subsidy regime,” Sanusi said.

“PMS import volumes have fallen from an average of 57 million litres/day in 2011 to 35 million litres/day in 2016. This is an achievement. The next step should be a full and unequivocal elimination of subsidy regime.”

Source: NBS

FIX FAILURES IN THE POWER SECTOR VALUE CHAIN, STARTING WITH DISCOs

Sanusi said the president’s team must “petition for a specific debt raising programme to address unpaid arrears. Until this happens no new investment can take place”.

“Raise public awareness about the necessity of cost-reflective tariffs, including the hike in 2016. Raise fresh capital to pay off arrears to Gencos. These are N235bn and building. The higher the tariffs go (as they are bound to do) the more quickly they will build,” he said.

“Until these backlogs are paid, no one is going to invest in new generation capacity. Force Disco owners to make stipulated investments in metering. What I’m told is that many disco owners have failed to honour their terms of the agreement, both in investing in metering and upgrading the old infrastructure.

“Until this failure in the value chain is addressed, collection rates will never be good enough to achieve cost recovery, and the government/NBET will always be on the hook for the shortfall.”

He also called for a resolution of gas supply issues.

DIGITISE STATE LAND REGISTRIES, STREAMLINE RELEVANT LEGISLATION

Quoting World Bank’s Doing Business index, Sanusi said: “Nigeria remains one of the most difficult countries in which to register property. State governments can do something about this.

“In fact, Lagos State has already taken great strides towards simplifying the procedure of registering land by merging all relevant laws into a single piece of legislation.”

He asked that land registries be taken online and made easier for businesses in Nigeria.

RE-PRIORITISE PUBLIC SPENDING TOWARDS INVESTMENT IN HUMAN CAPITAL

“In Nigeria, the public sector wage bill went up from N443bn in 2005 to N1.659 trillion in 2012, driven by a 53% increase in civil servants’ wages in 2010,” he said.

“The government has consistently prioritised recurrent expenditure over investment – all the more so in times of economic difficulty and leading up to elections.”

He called for investment in human capital if Nigeria must make its way out of this economic quagmire.

PRIVATE SECTOR INVESTMENT IN CAPITAL EXPENDITURE

“The economy has quadrupled in nominal terms since 2005, and the population has grown by over 40 million, but capex has barely changed.

“The major problem for Nigeria is revenue. Across all 3 levels of government, it collected just US$117 per person in 2015, and invested US$17. Kenya, with half of Nigeria’s level of wealth on paper, collected almost twice as much in taxes.

“If Nigeria is going to adopt an investment-driven model, it cannot rely on the public sector alone.”

Sanusi urged Buhari’s men to let the private sector also drive investment.

SET FX RATE TO INCENTIVISE CAPITAL INFLOWS, CATALYSE FDI

“Nigeria has made dramatic changes to its FX regime, moving from a hard peg to a free float. These bold steps have gone a long way to restoring its credibility.

“On a trade and inflation weighted basis, the naira has gone from one of the most over-valued currencies in the world to one that is now under-valued.

“A major barrier to bringing capital in from abroad has been removed; a major incentive to take capital out has also been removed.”

He said such incentives must be maintained as government set interest rates at levels that deter capital flight, dollarization.

BEWARE OF CHINA… PROTECT INFANT INDUSTRIES

“Beyond fixing the basic supply side issues, Nigeria also needs to take measures to protect its infant industries.

“Large surplus countries like China have been using the promise of investment and cheap debt to gain unfettered access to Africa’s local markets.

“But the relationship has become imbalanced. Without manufacturing capacity of its own, Africa can never provide meaningful employment for its youth.

“Successful policies in cement and auto assembly should be replicated for petro-chemicals and agro-processing.”

He concluded that government must get the appropriate macro policies in place and create a supportive business environment.

Follow us on twitter @thecableng

Copyright 2016 TheCable. Permission to use quotations from this article is granted subject to appropriate credit being given to www.thecable.ng as the source.

Copyright 2016 TheCable. Permission to use quotations from this article is granted subject to appropriate credit being given to www.thecable.ng as the source.

No comments:

Post a Comment